Rising patient out-of-pocket costs are a direct threat to your practice’s financial health. When patients can’t pay their high-deductible balances in full, those accounts often become uncollectible bad debt. The solution is a structured patient payment plan program.

By the Numbers: Practices that implement formal payment plans collect up to 70% more on outstanding patient balances, turning potential write-offs into predictable revenue.

For a practice owner, the benefits extend far beyond improved collections. A well-run program strengthens patient relationships, reduces administrative workload, and creates the kind of predictable cash flow that is critical for strategic planning. Most importantly, it significantly enhances your practice’s value.

How Do Payment Plans Impact Your Practice’s Financial Health and Valuation?

Implementing a payment plan program is a strategic business decision that directly impacts your bottom line. Instead of writing off large balances, you convert them into manageable monthly installments. This simple shift can reduce bad debt by 30-50%, directly adding to your net revenue. This approach also lowers collection costs, as automated plans are far more efficient than manual follow-ups or costly third-party agencies.

From a valuation perspective, a formal program is a powerful asset. During a sale or merger, buyers analyze your revenue cycle for risk and predictability.

Pro-Tip for Practice Owners: Potential buyers view a sophisticated payment plan system as a sign of strong operational management and a reliable revenue stream, leading to higher valuations during financial due diligence.

A practice with a documented, high-performing payment plan program demonstrates predictable revenue, a lower risk profile, and strong patient retention—all factors that help justify a premium valuation.

Is It Standard for Medical Practices to Offer Payment Plans?

Yes, offering payment plans has become an industry standard. Approximately 90% of hospitals and 75% of private practices provide some form of payment arrangement. The key differentiator for a high-value practice is not if you offer plans, but how structured, consistent, and efficient your program is.

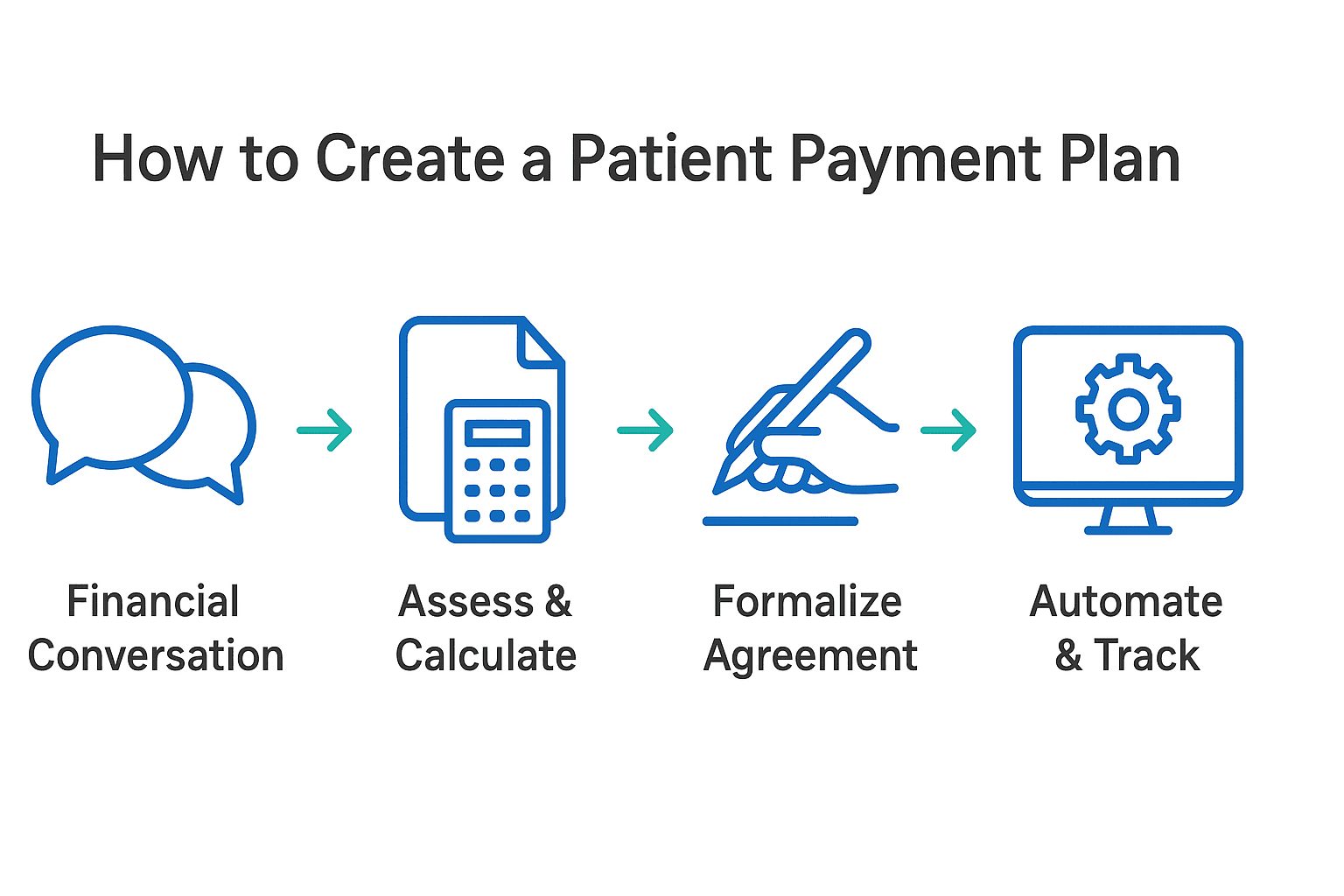

How Do You Create a Patient Payment Plan?

Creating a payment plan should be a systematic process, not an improvised one. Train your staff to follow a clear, empathetic workflow that begins with a proactive financial conversation. Next, assess the patient’s financial situation to determine a realistic monthly payment. With this information, calculate the terms and formalize the arrangement in a written agreement signed by both parties.

Key to Success: Mandating automatic payments via bank withdrawal (ACH) or a credit card on file is the single most effective step to ensure compliance and reduce missed payments.

Once the agreement is signed and payment is configured, enter the plan into your practice management software to automate tracking and reminders.

What Should Your Office Payment Plan Policy Include?

A clear, written policy is essential for consistency, fairness, and legal protection. It empowers your staff to make decisions within a defined framework and must be applied equally to all patients. Here are the core components to define:

| Policy Component | Recommended Guideline |

| Minimum Balance | Set a threshold of $200 – $500. Balances below this should be paid in full within 30-60 days. |

| Down Payment | Require 10-20% of the total balance upfront to secure patient commitment and immediately reduce the principal. |

| Plan Lengths | Establish standard durations based on balance size (e.g., up to 12 months for <$1,000; 12-24 months for >$1,000). |

| Interest | Offer interest-free plans to avoid complex Truth in Lending Act (TILA) regulations. It’s simpler and better for patient relations. |

| Payment Method | Mandate automatic payments (ACH or credit card on file) as the default. This reduces missed payments by over 60%. |

| Default Conditions | Define a 10-15 day grace period and specify that a plan defaults after 2-3 consecutive missed payments. |

| Approval Authority | Define who can approve plans at different balance levels (e.g., front desk up to $1,000, office manager up to $5,000). |

What Technology Do You Need to Manage Payment Plans?

Managing payment plans effectively is impossible with spreadsheets. Investing in the right technology is critical for efficiency and success. Your practice management system (PMS) may have built-in modules for this purpose. If its capabilities are limited, consider dedicated payment plan software.

The core of your technology stack must be a non-negotiable, PCI-compliant system. This should be complemented with automated communication tools that send email and SMS reminders. A patient portal that provides 24/7 self-service access is also a key component. Ensure any technology you choose integrates seamlessly with your EHR and accounting software to maintain a single source of financial truth.

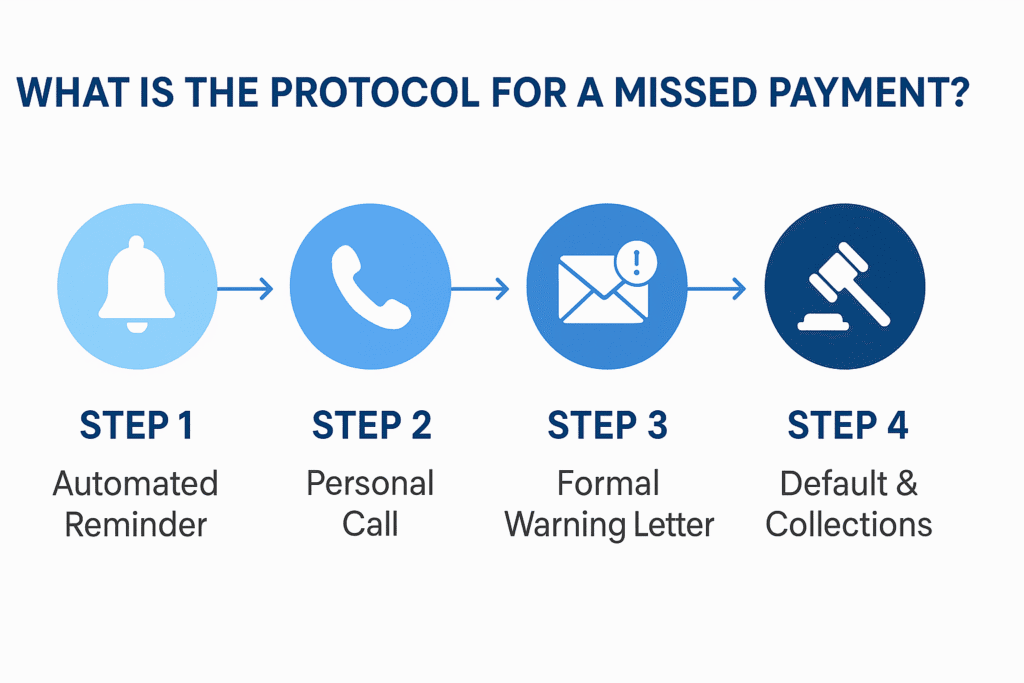

What Is the Protocol for a Missed Payment?

Even with a great system, missed payments will happen. Your response should be systematic and escalate appropriately. The process should begin with a grace period and an automated reminder. If that fails, a staff member should place a personal phone call to understand the situation.

Strategic Insight: It is often better to modify a struggling patient’s plan than to force a default. Flexibility improves long-term collection rates and preserves the patient relationship.

If the patient remains non-responsive after a second missed payment, send a formal written warning letter. The final step is to declare the plan in default according to your policy, making the full balance due and eligible for collections.

What Legal and Compliance Issues Must You Consider?

Navigating payment plans requires an awareness of several key regulations. HIPAA rules govern how you share information, while federal laws like the Truth in Lending Act (TILA), Fair Debt Collection Practices Act (FDCPA), and the Equal Credit Opportunity Act (ECOA) set strict guidelines. Most importantly, ensure your policies do not inadvertently violate Stark Law and Anti-Kickback regulations.

Disclaimer: This information is for educational purposes and is not legal advice. Consult with an attorney familiar with healthcare and consumer credit laws in your state to ensure your policies are compliant.

What Are Your Next Steps?

An effective payment plan program is a cornerstone of a modern, financially resilient healthcare practice. To move forward, first assess your current process. From there, draft a formal, written policy and have it reviewed by legal counsel. Simultaneously, evaluate your technology to determine if your current system is sufficient. Once your policy and tools are in place, train your team on the new procedures. Finally, launch the program and begin tracking key metrics to monitor performance and make continuous improvements.

About SovDoc: We are healthcare M&A specialists who have guided hundreds of practice owners through successful sales and partnerships. We consistently see that practices with sophisticated revenue cycle management—including well-structured patient payment programs—achieve higher valuations. These systems demonstrate predictable revenue, strong patient relationships, and professional management. If you are considering a future exit or want to build a more valuable practice, contact our team to learn how we can help you prepare for your next chapter.